Bebeto Matthews/AP WASHINGTON -- Consumer confidence in the U.S. economy fell in November to the lowest level in seven months, dragged down by greater concerns about hiring and pay in the coming months. The Conference Board said Tuesday that its index of consumer confidence dropped to 70.4 from 72.4 in October. The October reading was higher than initially reported, but still well below the 80.2 reading in September. Confidence plunged in October on worries about the shutdown. The November decline, however, was mostly due to concerns about the next six months. Less optimism among Americans could slow the holiday shopping season and weigh on economic growth. Consumer spending drives 70 percent of economic activity. But spending patterns don't always closely follow measures of confidence. Americans sometimes shop more even when they say they are less optimistic. That's what happened last month. Despite a sharp fall in confidence in October, consumers spent 0.4 percent more at retail stores and restaurants than in September. Strong auto sales accounted for about half the gain. Restaurants also reported a healthy increase in spending. Americans also spent more on furniture, electronics and clothing. There were some signs of caution: sales at grocery stores were flat and department stores reported only slightly higher sales. Lower gas prices and a recent pickup in job gains could help maintain Americans' ability to spend, even as their confidence wanes. Employers added an average of 202,000 jobs from August through October, up from just 146,000 in the previous three months. And lower gas prices have put more money in consumers' pockets. Prices fell for nine straight weeks to the lowest level in nearly two years before moving up slightly in the past two week. The average price for a gallon of gas nationwide Monday was $3.28. Economic growth is expected to slow in the current October-December quarter, partly because consumer spending growth is likely to be moderate. The economy expanded at a 2.8 percent annual rate in the July-September quarter, but most economists expect it will slow to about a 2 percent rate or lower in the fourth quarter.

Bebeto Matthews/AP WASHINGTON -- Consumer confidence in the U.S. economy fell in November to the lowest level in seven months, dragged down by greater concerns about hiring and pay in the coming months. The Conference Board said Tuesday that its index of consumer confidence dropped to 70.4 from 72.4 in October. The October reading was higher than initially reported, but still well below the 80.2 reading in September. Confidence plunged in October on worries about the shutdown. The November decline, however, was mostly due to concerns about the next six months. Less optimism among Americans could slow the holiday shopping season and weigh on economic growth. Consumer spending drives 70 percent of economic activity. But spending patterns don't always closely follow measures of confidence. Americans sometimes shop more even when they say they are less optimistic. That's what happened last month. Despite a sharp fall in confidence in October, consumers spent 0.4 percent more at retail stores and restaurants than in September. Strong auto sales accounted for about half the gain. Restaurants also reported a healthy increase in spending. Americans also spent more on furniture, electronics and clothing. There were some signs of caution: sales at grocery stores were flat and department stores reported only slightly higher sales. Lower gas prices and a recent pickup in job gains could help maintain Americans' ability to spend, even as their confidence wanes. Employers added an average of 202,000 jobs from August through October, up from just 146,000 in the previous three months. And lower gas prices have put more money in consumers' pockets. Prices fell for nine straight weeks to the lowest level in nearly two years before moving up slightly in the past two week. The average price for a gallon of gas nationwide Monday was $3.28. Economic growth is expected to slow in the current October-December quarter, partly because consumer spending growth is likely to be moderate. The economy expanded at a 2.8 percent annual rate in the July-September quarter, but most economists expect it will slow to about a 2 percent rate or lower in the fourth quarter.

Friday, January 31, 2014

Consumer Confidence Falls to 7-Month Low

Fewer Americans Traveling This Year for Thanksgiving

Alex Brandon/AP NEW YORK -- Fewer Americans will travel during the Thanksgiving holiday weekend as economic uncertainty in a sluggish recovery curbs travel plans, travel group AAA said Wednesday. AAA expects 38.9 million Americans to drive 50 miles or more from their homes for the holiday period, which is from Wednesday, Nov. 27, to Sunday, Dec. 1, a decline of 1.6 percent from the 2012 holiday period and would come despite falling fuel prices, AAA noted. About 3.14 million will fly to their destinations, a 3.7 percent drop from 2012, according to AAA. Approximately 1.4 million will use other modes of transportation, including rail, bus or cruise ship, putting the total number of expected Thanksgiving travelers at 43.4 million, down 1.5 percent from 2012, AAA said. "While the economy continues to improve, the sluggish pace of the recovery is creating uncertainty in the minds of some consumers, and therefore AAA is projecting a slight decline in the number of Thanksgiving travelers this year," Marshall Doney, AAA chief operating officer, said in a release. The slip in expected travel by automobile comes even with gasoline prices "at their lowest levels for the holiday since 2010," Doney noted. The U.S. average retail price for regular gasoline stood at $3.209 a gallon Tuesday, according to AAA, down from $3.416 a gallon a year ago. AAA said it expects drivers in the majority of states to be able to find fuel stations selling gasoline for less than $3 a gallon.

Alex Brandon/AP NEW YORK -- Fewer Americans will travel during the Thanksgiving holiday weekend as economic uncertainty in a sluggish recovery curbs travel plans, travel group AAA said Wednesday. AAA expects 38.9 million Americans to drive 50 miles or more from their homes for the holiday period, which is from Wednesday, Nov. 27, to Sunday, Dec. 1, a decline of 1.6 percent from the 2012 holiday period and would come despite falling fuel prices, AAA noted. About 3.14 million will fly to their destinations, a 3.7 percent drop from 2012, according to AAA. Approximately 1.4 million will use other modes of transportation, including rail, bus or cruise ship, putting the total number of expected Thanksgiving travelers at 43.4 million, down 1.5 percent from 2012, AAA said. "While the economy continues to improve, the sluggish pace of the recovery is creating uncertainty in the minds of some consumers, and therefore AAA is projecting a slight decline in the number of Thanksgiving travelers this year," Marshall Doney, AAA chief operating officer, said in a release. The slip in expected travel by automobile comes even with gasoline prices "at their lowest levels for the holiday since 2010," Doney noted. The U.S. average retail price for regular gasoline stood at $3.209 a gallon Tuesday, according to AAA, down from $3.416 a gallon a year ago. AAA said it expects drivers in the majority of states to be able to find fuel stations selling gasoline for less than $3 a gallon.

Sony Corporation (ADR) (SNE): PS4 Google Trending In The Right Direction

Today is the day that gamers will be able to purchase Sony Corporation's (SNE) PlayStation 4 a.k.a. PS4. It's the generational upgrade since PlayStation 3 was released in the US in 2006. This version will be priced at $399.

As we like to do with much anticipated, new product releases, iStock checked Google Trends to see if we can get a sense of how popular the PS4 will be with consumers. So, we compared search volume intensity for the keywords "PS3" and "PS4"

PlayStation 3 was available for sale on November 17, 2006. At the time, SNE was trading around $40 per share. On May 22, 2007, Sony shares hit an intra-day, 52-week high of $59.84. Obviously, shareholders were happy to ride the success of PS3 for nearly a 50% gain.

[Related -Futures Down Amid Lack Of Catalysts; International Business Machines Corp. (IBM) In Focus]

The question is whether PS4 will follow PS3's success, blaze its own trail, or dash the hopes of investors.

On November 17, 2006, search volume intensity for PS3 peaked at a score of 60 out of 100. Fast forward to today and we find that web queries for PS4 are reaching their high, but about a third less than PS3's November score.

iStock anticipates that PlayStation 4's score will continue its vertical ascent tomorrow. PS3 saw its search volume intensity jump by 69.5% on launch-day verses launch-eve. If the same trend holds, then PS4 should push a Google Trend score of close to 70, which could mean that PS4 will have a more successful start than PS3.

[Related -Sony Options Active As Shares Hit Fresh 52-Week High]

Sony's stock chart shows that investors are gearing up for a hot start. SNE shares have jumped a couple of bucks in the past few days. Wall Street's interest appears to be building as volume is stepping up as tomorrow approaches. In fact, yesterday was one of the top 10 active days for 2013.

The enthusiasm helped create a bullish MACD crossover, which has been a reliable buy signal for SNE shares in the past year; four-! out-of-four times, Sony's share price increased immediately afterwards. This time, PS4 could prove to be the catalyst that makes it five-for-five.

Overall: Google Trends suggest that PlayStation 4 should be well received by consumers. iStock does have some concerns as PS3 was initially sold at less than what it cost to build the console. If Sony applies the same model again, then margins and the stock could take a hit, which is exactly what happened in 2006 before Sony Corporation's (SNE) embarked on its 50% march higher.

Thursday, January 30, 2014

2 Drug Promotions Going in Opposite Directions

When a drug is struggling to reach its full potential, companies have two options: double down and try to sell more or scale back and try to get expenses in line with the revenue the drug is bringing in.

This month we've seen drugmakers take both approaches. Arena Pharmaceuticals' (NASDAQ: ARNA ) marketing partner Eisai is doubling the sales force that sells the duo's obesity drug Belviq. Meanwhile, Amarin (NASDAQ: AMRN ) , which sells lipid-lowering Vascepa, said it's going to reduce its headcount by 50%.

Money matters

The biggest difference between Arena Pharmaceuticals and Amarin is that Arena has a big pharma partner. Eisai is in charge of selling the drug, and Arena simply collects manufacturing revenue on sales of the drug.

If Arena had to pay for the entire sales force itself, I don't know that it would be expanding right now; the added cost isn't likely to be recouped any time soon.

For example, Qsymia, the other new obesity drug, had net sales of $5.5 million in the second quarter, and VIVUS (NASDAQ: VVUS ) spent almost $43 million on sales, marketing, and general expenses. Granted that includes more than just the sales force, but it's clear VIVUS has a ways to go before it'll be profitable.

The expenses are a long-term investment in growing sales for VIVUS and Eisai. Before Belviq and Qsymia were approved, the obesity market hadn't seen a new drug in a decade and had more than one get pulled off the market because of safety concerns. Getting doctors to come around is going to take time, but it seems reasonable to assume that a larger sales force will accomplish that goal quicker.

Short-sighted?

It's going to be hard for Amarin to grow sales of Vascepa with a slimmed down sales force, but the company has to be a bit short-sighted at this point. The remaining sales force will target the doctors that are most likely to prescribe Vascepa, maximizing their contribution to profits from the drug.

Amarin was counting on the FDA expanding Vascepa's indication to include patients with moderately high triglyceride levels -- it's currently only approved for treating patients with extremely high triglyceride levels -- but there appears to be no chance of the FDA approving the expanded indication.

At this point, Amarin's only goal is to survive until the company gets data from its outcomes study and can reapply to the FDA. The large trial isn't cheap, so conserving cash is important. Amarin can always ramp its sales force back up -- or, more likely, find a big pharma partner -- if the outcomes trial is positive.

Game-changing biotechs

The best way to play the biotech space is to find companies that shun the status quo and instead discover revolutionary, groundbreaking technologies. In The Motley Fool's brand-new FREE report "2 Game-Changing Biotechs Revolutionizing the Way We Treat Cancer," find out about a new technology that big pharma is endorsing through partnerships, and the two companies that are set to profit from this emerging drug class. Click here to get your copy today.

U.S. seeks $2.1 billion from Bank of America

The federal government is seeking $2.1 billion in fines from Bank of America.

NEW YORK (CNNMoney) The Justice Department is seeking $2.1 billion in fines from Bank of America related to mortgage fraud perpetrated by Countrywide Financial before it was purchased by BofA.The amount is a significant increase from the previous request for $863 million.

The case involved mortgages sold in 2007 and early 2008 to Fannie Mae and Freddie Mac, the two government-backed mortgage finance companies. The loans were made under a Countrywide program known as the "High-Speed Swim Lane" but were known internally at the lender as "the Hustle" according to the Justice Department.

A jury found Bank of America guilty of fraud last October in a civil case involving Countrywide's actions. Bank of America (BAC, Fortune 500) acquired Countrywide in 2008.

In the motion filed late Wednesday, the government argues that Countrywide's gross proceeds from the sale of mortgage loans involved in the case topped $5 billion and that experts have determined 43% of those loans were "defective and sold with misrepresentations."

The case was originally brought by Edward O'Donnell, a former Countrywide executive who claims to have complained repeatedly about loan quality standards at the firm. O'Donnell, who could be awarded up to $1.6 million in the case, filed the suit under federal whistleblower laws and the Justice Department later joined.

Why big banks are too big to jail

Why big banks are too big to jail Bank of America spokesman Lawrence Grayson said the gross loss on the loans was only the $863 million that the government had previously requested and that the net loss after the foreclosed properties were sold by the lenders was only $130 million.

"This claim bears no relation to a limited Countrywide program that lasted several months and ended before Bank of America's acquisition of Countrywide," said Grayson. "We will present the relevant facts in a detailed response soon."

A hearing on the fines is set for March 13.

Early last year Bank of America reached a separate $10.3 billion settlement with Fannie M! ae to deal with questionable home loans it sold to Fannie.

-- CNNMoney's James O'Toole contributed to this report ![]()

5 Stocks Insiders Love Right Now

DELAFIELD, Wis. (Stockpickr) -- Corporate insiders sell their own companies' stock for a number of reasons.

>>The Pros Hate These 5 Stocks -- Should You?

They might need the cash for a big personal purchase such as a new house or yacht, or they might need the cash to fund a charity. Sometimes they sell as part of a planned selling program that they have put in place for diversification purposes, which allows them to sell stock in stages instead of selling all at one price.

Other times they sell because they think their stock is overvalued and the risk/reward is no longer attractive. Some even dump their own stock because they have inside knowledge that a competitor is eating their lunch and stealing market share.

But insiders usually buy their own shares for one reason: They think the stock is a bargain and has tremendous upside.

>>5 Stocks Under $10 to Trade for Breakouts

The key word in that last statement is "think." Just because a corporate insider thinks his or her stock is going to trade higher, that doesn't mean it will play out that way. Insiders can have all the conviction in the world that their stock is a buy, but if the market doesn't agree with them, the stock could end up going nowhere. Also, I say "usually" because sometimes insiders are loaned money by the company to buy their own stock. Those loans are often sweetheart deals and shouldn't be viewed as organic insider buying.

At the end of the day, its large institutional money managers running big mutual funds and hedge funds that drive stock prices, not insiders. That said, many of these savvy stock operators will follow insider buying activity when they agree with the insider that the stock is undervalued and has upside potential. This is why it's so important to always be monitoring insider activity, but it's twice as important to make sure the trend of the stock coincides with the insider buying.

>>5 Rocket Stocks to Buy Now

Recently, a number of companies' corporate insiders have bought large amounts of stock. These insiders are finding some value in the market, which warrants a closer look at these stocks. Here's a look at five stocks whosed insiders have been doing some big buying per SEC filings.

SolarCity

One renewable energy player that insiders are snapping up a huge amount of stock in here is SolarCity (SCTY), which is engaged in designing, sales, engineering, installation, monitoring, maintenance and financing of solar energy systems to residential and commercial customers, and sale of electricity generated by solar energy systems to customers. Insiders are buying this stock into major strength, since shares are up 375% so far in 2013.

>>5 Stocks Poised for Breakouts

SolarCity has a market cap of $4.4 billion and an enterprise value of $4.7 billion. This stock trades at a premium valuation, with a price-to-sales of 37.33 and a price-to-book of 25.70. Its estimated growth rate for this year is 67.4%, and for next year it's pegged at 1.2%. This is not a cash-rich company, since the total cash position on its balance sheet is $159.61 million and its total debt is $299.36 million.

A director just bought 214,869 shares, or $10 million worth of stock, at $46.54 a share. The CEO also just bought 107,434 shares, or about $4.99 million worth of stock, at $46.54 a share. An officer also just bought 107,434 shares, or about $4.99 million worth of stock, at $46.54 a share.

From a technical perspective, SCTY is currently trending above both its 50-day and 200-day moving averages, which is bullish. This stock has been uptrending strong for the last two months, with shares soaring higher from its low of $28.31 to its recent high of $64.50 a share. During that uptrend, shares of SCTY have been making mostly higher lows and higher highs, which is bullish technical price action. That move has now pushed shares of SCTY into overbought territory, since its current relative strength index reading is 72.

If you're bullish on SCTY, then I would look for long-biased trades off a significant pullback, since this stock is too extended above both its 50-day and 200-day moving averages. This stock has put in a major run recently, so it would be wise to wait for lower prices before initiating any new long positions. Some possible buy areas could be around $50 to $45 a share. Let this stock cool off first and base for a bit before jumping in.

Acorn Energy

Another technology player that insiders are active in here is Acorn Energy (ACFN), which provides digital solutions for energy infrastructure asset management. Insiders are buying this stock into major weakness, since shares are off by 56% so far in 2013.

>>5 Dogs of the Dow to Stomp the Market

Acorn Energy has a market cap of $62 million and an enterprise value of $45 million. This stock trades at a reasonable valuation, with a price-to-sales of 2.98 and a price-to-book of 1.56. Its estimated growth rate for this year is -11.8%, and for next year it's pegged at 50%. This is a cash-rich company, since the total cash position on its balance sheet is $13.35 million and its total debt is just $251,000. This stock currently sports a 4.3% dividend yield.

A director just bought 80,000 shares, or $228,000 worth of stock, at $2.85 per share.

From a technical perspective, ACFN is currently trending below both its 50-day and 200-day moving averages, which is bearish. This stock has been downtrending badly for the last four months, with share plunging from its high of $9.90 to its recent low of $2.85 a share. During that downtrend, shares of ACFN have been consistently making lower highs and lower lows, which is bearish technical price action. That said, shares of ACFN have now entered oversold territory, since its current relative strength index reading is 33.31. Oversold can always get more oversold, but it's also an area where a stock can rebound sharply higher from.

If you're in the bull camp on ACFN, then look for long-biased trades as long as this stock is trending above some near-term support at $3.21 and then once it breaks out above some near-term overhead resistance at $3.59 a share with high volume. Look for a sustained move or close above that level with volume that hits near or above its three-month average action of 213,249 shares. If that breakout triggers soon, then ACFN will set up to re-test or possibly take out its next major overhead resistance levels at $4.50 to its 50-day moving average at $5.37 a share. This stock could even hit $6 if we see big volume move in here on that breakout.

EV Energy Partner LP

One energy player that insiders are jumping into big here is EV Energy Partner LP (EVEP), which is engaged in the development and production of oil and natural gas properties. Insiders are buying this stock into big weakness, since shares are down by 33% so far in 2013.

>>5 Hated Earnings Stocks You Should Love

EV Energy Partner LP has a market cap of $1.6 billion and an enterprise value of $2.5 billion. This stock trades at a cheap valuation, with a forward price-to-earnings of 25.67. Its estimated growth rate for this year is 155.3%, and for next year it's pegged at 595.2%. This is not a cash-rich company, since the total cash position on its balance sheet is $8.28 million and its total debt is $1.02 billion. This stock currently sports a dividend yield of 8.4%.

The chairman of the board just bought 135,000 shares, or about $4.97 million worth of stock, at $36.86 per share. The CEO also just bought 15,000 shares, or about $552,000 worth of stock, at $36.86 per share.

From a technical perspective, EVEP is currently trending above its 50-day moving average and well below its 200-day moving average, which is neutral trendwise. This stock has been trending sideways and consolidating over the last two months and change, with shares moving between $34.01 on the downside and $39.74 on the upside. Shares of EVEP have just started to trend back above its 50-day moving average, and it's quickly moving within range of triggering a breakout trade above the upper-end of its sideways chart pattern.

If you're bullish on EVEP, then look for long-biased trades as long as this stock is trending above some key near-term support levels at $36.55 or at $35.60 and then once it breaks out above some near-term overhead resistance levels at $38.94 to $39.74 a share with high volume. Look for a sustained move or close above those levels with volume that hits near or above its three-month average volume of 254,366 shares. If that breakout triggers soon, then EVEP will set up to re-test or possibly take out its next major overhead resistance levels at $42 to $42.50, or even its 200-day moving average of $43.29 a share.

Ryman Hospitality Properties

One REIT player that insiders are in love with here is Ryman Hospitality Properties (RHP), which operates as a real estate investment trust specializing in group-oriented, destination hotel assets in urban and resort markets. Insiders are buying this stock into notable weakness, since shares are off by 14% during the last six months.

>>5 Big Stocks to Trade for Big Gains

Ryman Hospitality Properties has a market cap of $1.8 billion and an enterprise value of $2.9 million. This stock trades at a premium valuation, with a trailing price-to-earnings of 86.47 and a forward price-to-earnings of 27.94. Its estimated growth rate for this year is 400%, and for next year it's pegged at -20.2%. This is not a cash-rich company, since the total cash position on its balance sheet is $44.40 million and its total debt is $1.15 billion. This stock currently sports a dividend yield of 5.5%.

The CEO just bought 6,682 shares, or about $232,000 worth of stock, at $34.79 per share.

From a technical perspective, RHP is currently trending above its 50-day moving average and just below its 200-day moving average, which is neutral trendwise. This stock has been uptrending strong over the last two months, with shares moving higher from its low of $32.50 to its recent high of $37.96 a share. During that move, shares of RHP have been making mostly higher lows and higher highs, which is bullish technical price action. That move has now pushed shares of RHP within range of triggering a big breakout trade.

If you're bullish on RHP, then look for long-biased trades as long as this stock is trending above some near-term support at $36 and then once it breaks out above some near-term overhead resistance levels at its 50-day of $38.43 to some past resistance at $38.74 a share with high volume. Look for a sustained move or close above those levels with volume that hits near or above its three-month average volume of 795,155shares. If that breakout triggers soon, then RHP will set up to re-test or possibly take out its next major overhead resistance levels at $42 to $44 a share, or even $47 a share.

Accelrys

One final name with some large insider buying is Accelrys (ACCL), which develops and commercializes scientific business intelligence software and solutions that enable its customers to accelerate the discovery and development of new drugs and materials. Insiders are buying this stock into modest strength, since shares are up 7.9% so far in 2013.

Accelrys has a market cap of $542 million and an enterprise value of $404 million. This stock trades at a premium valuation, with a trailing price-to-earnings of 85.70 and a forward price-to-earnings of 25.71. Its estimated growth rate for this year is -8.6%, and for next year it's pegged at 18.8%. This is a cash-rich company, since the total cash position on its balance sheet is $130.84 million and its total debt is zero.

A beneficial owner just bought 200,000 shares, or about $1.88 million worth of stock, at $9.40 per share.

From a technical perspective, ACCL is currently trending above both its 50-day and 200-day moving averages, which is bullish. This stock has been uptrending strong for the last five months, with shares moving higher from its low of 8.03 to its recent high of $10 a share. During that uptrend, shares of ACCL have been consistently making higher lows and higher highs, which is bullish technical price action. That move has now pushed shares of ACCL within range of triggering a big breakout trade.

If you're bullish on ACCL, then look for long-biased trades as long as this stock is trending above its 50-day at $9.43 or its 200-day at $9.19 and then once it breaks out above some near-term overhead resistance at $9.90 a share to its 52-week high at $10 a share with high volume. Look for a sustained move or close above those levels with volume that hits near or above its three-month average action of 121,560 shares. If that breakout triggers soon, then ACCL will set up to enter new 52-week-high territory, which is bullish technical price action. Some possible upside targets off that breakout are $13 to $15 a share.

To see more stocks with notable insider buying, check out the Stocks With Big Insider Buying portfolio on Stockpickr.

-- Written by Roberto Pedone in Delafield, Wis.

RELATED LINKS:

>>4 Financial Stocks Rising on Big Volume

>>4 Stocks Under $10 Spiking Higher

>>Do You Own These Blue-Chips? Sell Them!

Follow Stockpickr on Twitter and become a fan on Facebook.

At the time of publication, author had no positions in stocks mentioned.

Roberto Pedone, based out of Delafield, Wis., is an independent trader who focuses on technical analysis for small- and large-cap stocks, options, futures, commodities and currencies. Roberto studied international business at the Milwaukee School of Engineering, and he spent a year overseas studying business in Lubeck, Germany. His work has appeared on financial outlets including

CNBC.com and Forbes.com. You can follow Pedone on Twitter at www.twitter.com/zerosum24 or @zerosum24.Wednesday, January 29, 2014

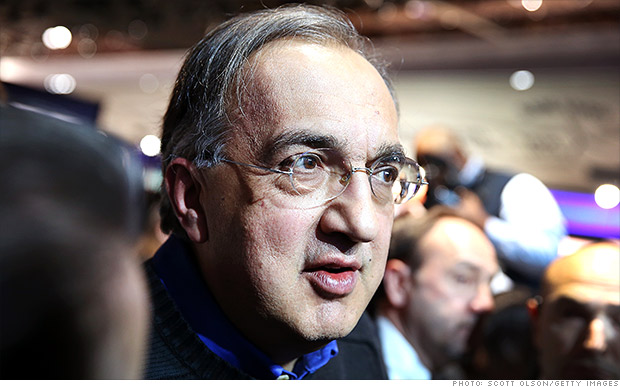

Chrysler parent is renamed Fiat Chrysler Automobiles

Sergio Marchionne is CEO of the newly named Fiat Chrysler Automobiles.

NEW YORK (CNNMoney) The reorganized Fiat and Chrysler Group got a new name - Fiat Chrysler Automobiles - and a new legal home on neutral territory in the Netherlands, the company announced Wednesday.The company will not actually have offices based in the Netherlands, the same way many U.S. corporations are incorporated in Delaware without actually having any operations there. Instead Chrysler will continue to operate out of its current home in the Detroit suburb of Auburn Hills, Mich., while Fiat will remain in its current Milan headquarters. Shares of the company will trade on both the New York Stock Exchange and in Milan. And for purposes of taxation, the company will be based in the U.K., not any of the three countries it now calls home.

The company also unveiled a new logo with the initials FCA. "Use of an acronym helps create a transition from the past, without severing the roots," said the company.

Sergio Marchionne, who has served as CEO of both Fiat and Chrysler since Fiat bought a controlling stake in Chrysler out of bankruptcy court in 2009, said the new corporate home will help the company's access to global financial markets.

"Today we can say that we have succeeded in creating solid foundations for a global automaker with a mix of experience and know-how on a level with the best of our competitors," he said. "An international governance structure and listings will complete this vision."

The merger of the two companies became final earlier this month, when Fiat reached an agreement to buy the remaining shares of Chrysler from a union-controlled trust fund. But it will take some time before Fiat Chrysler shares trade in New York again. All the company would say is that they will trade some time before the end of the year.

The costs associated with closing the merger forced Fiat Chrysler to suspend its dividend. That and disappointing earnings and guidance caused shares of Fiat Group to fall more than 5% in Milan trading on Wednesday.

In addition to the two mass-market brands, Chrysler and Fiat, the company also makes high-price performance vehicles under the Maserati, Ferrari and Alfa Romeo brands.

Chrysler accounted for about 55% of the combined company's 4.4 million vehicle sales in 2013. It accounted for all of the companies' profits last year, as ongoing losses in Europe wiped out earnings outside North America. ![]()

Tuesday, January 28, 2014

Jim Cramer's 6 Stocks in 60 Seconds: VZ AMD BHI BAX AMZN UNH (Update 1)

Check out Jim Cramer's latest trading recommendations on "Action Alerts Plus". (Updates from 10:32 a.m. ET with closing information.)

NEW YORK (TheStreet) -- Here's what Jim Cramer had to say on CNBC's "Squawk on the Street" Friday.

Cramer said Verizon (VZ) keeps getting the love from analysts, this time from Deutsche Bank, which upgraded the stock to buy from hold. VZ closed up 2.3% to $50.01.

Advanced Micro Devices (AMD) missed on earnings. Cramer said it was a bad report, mainly due to poor PC sales. AMD dropped 13.7% to $3.53. Baker Hughes (BHI) reported a "magnificent number," according to Cramer. He thinks the company may have finally gotten it together. BHI jumped 7.3% to $55.55. Raymond James downgraded Baxter International (BAX) to hold from buy. Cramer said it makes sense for the company to split up since it essentially has two different businesses. BAX closed 1.8% lower at $66. Amazon (AMZN) is higher because UBS said e-commerce is doing well, contradicting what eBay (EBAY) said on its conference call. Cramer suggested that perhaps "it's raining on eBay's side of the street." AMZN rose 5.8% to $328.93. Cantor Fitzgerald downgraded UnitedHealth Group (UNH) to hold from buy. Cramer said the company reported surprisingly poor earnings results. UNH fell 3.7% to $68.76. To sign up for Jim Cramer's free Booyah! newsletter, with all of his latest articles and videos, please click here. -- Written by Bret Kenwell in Petoskey, Mich. Follow @BretKenwell

Monday, January 27, 2014

[video] Jim Cramer Quick Take: Get Defensive

NEW YORK (TheStreet) -- As the government shutdown continues without a resolution in sight, TheStreet's Jim Cramer told Debra Borchardt what investors should do in the current environment.

According to Cramer, some people just don't care what happens with the U.S. debt and wouldn't mind a default. Those people seem to think that's the price we need to pay and seem to have control of the House of Representatives, he added.

The political back-and-forth can wreak havoc on individual investors, but there's an alternative. Cramer, one of the few who has been against the government shutting down from the beginning, said investors could look to defensive sectors to weather the storm.

Bristol-Myers Squibb (BMY) can act as a rubric for what investors should be looking for in stocks, he said. Companies that are flush with cash and have no dependency on credit markets are the ones to be in when there's a risk of a default. Cramer concluded that investors should buy calls to limit risk and use stops to limit losses. This way, investors can risk less, while still having upside potential. -- Written by Bret Kenwell in Petoskey, Mich. Follow @BretKenwell

Sunday, January 26, 2014

Time For a New Back-Pain Treatment Paradigm (SYK, BRTX, MDT)

Just for the record, I'm not going to imply that BioRestorative Therapies, Inc. (OTCBB:BRTX) is poised to put companies like Medtronic (NYSE:MDT) or Stryker Corporation (NYSE:SYK). On the other hand, BioRestorative Therapies won't need to destroy Stryker Corporation or Medtronic to be rewarding for its shareholders. BRTX is only a $10 million company, and even the tiniest sliver of the spinal-related business that SYK or MDT are doing now could still be a windfall for shareholders of the up-and-coming organization.

At the heart of the matter, as was noted, is spinal care. Stryker and Medtronic are both well entrenched in the back business, which - by the way - is an industry worth about $10 billion per year. SYK owns about $1.4 billion worth of that market, selling its Aviator and Reflex spinal plates, and its more extensive OASYS bone-linking system. MDT is an even bigger player, selling about $3.2 billion worth of spinal fusion hardware like the INFUSE Bone Graft system.

All that skeletal technology is impressive to be sure, but ask any orthopedic or spinal surgeon... there is no simple or easy spinal surgery. All of them are invasive, can be painful, and require at least some post-surgery physical therapy. But, what if many of those surgeries could be sidestepped by a back-pain solution that was little more than an injection? Enter BioRestorative Therapies, Inc.

BRTX is the developer of a trio of stem cell therapies, but its flagship work is in the area of stem cell treatments for bulging and herniated discs. In some (read 'too many') cases where spinal fusions have been performed to reduce or eliminate back pain, had a viable spinal repair option been available, it may have sufficed. BioRestorative Therapies' brtxDISC program is potentially that viable option. Using a patient's own stem cells, a dose of healthy spinal disc cells is injected into a failing disc, which effectively repairs and rejuvenates the disc. It sure beats the heck out of screwing a hunk of metal onto a vertebrae, and physical therapy is rarely necessary.

Oh, it's a heck of a lot cheaper too... a reality BRTX expects to be able to easily capitalize on. The total cost for a stem cell disc treatment is about $18,000. Presumably the performing caregiver would charge for administering the treatment, but the grand total of a brtxDISC therapy is still going to be well shy of spinal fusions and discectomies, which can start at $35,000 and run all the way up to as much as $100,000 (and that doesn't factor in physical therapy). Insurance companies are going to love it to.

As for the opportunity at hand, BioRestorative Therapies estimates about one million candidates for the treatment option will surface every year. That's a multi-billion opportunity.

As for when it might become a reality, there's a chance the company may be able to skip Phase 1 trials and go straight to Phase 2, based on its preclinical/clinical work to date; 38 patients have already used this treatment approach, and the vast majority of them have seen their back pain significantly reduced. Only three of them went on to have other spinal surgeries after the BRTX treatment. Skipping Phase 2 trials could shave off a couple of years in the FDA's drug approval process. Even if the company does need to do a full-blown Phase 2 trial, though, veteran biotech investors know how this works - the market rewards milestones, not just reaching the end zone. Indeed, right now is the proverbial ground floor opportunity with this young company that could eventually shake things up a little for bigger players like Medtronic and Stryker.

If you'd like more trading ideas and insights like this one, become a subscriber to the SmallCap Network daily newsletter. You'll get stock picks, market calls, and more, FOR FREE! Sign up today.

Fact Check: Most Americans Still Have Free Checking Accounts

NEW YORK (LowCards.com) -- When the economic downturn hit five years ago, many analysts predicted free checking accounts would become a thing of the past. After all, regulations such as the CARD Act and Dodd-Frank bill cut some of the revenue streams of financial institutions, and many people thought banks would have to make up for this revenue with additional fees.

But the majority of Americans still enjoy a free checking account.

According to a survey conducted by the American Bankers Association, 55% of bank customers are not being charged a fee for their checking account.

The figures from the annual survey have hovered around that number for the past few years: 59% had a free checking account in 2011, and 53% in the 2010 survey. Also see: We're Getting More Confused by Credit Card Terms and Reward>> On the flip side, the findings show that almost half of Americans are now paying for a checking account. In fact, 14% pay $10 or more each month. Here are some tips to possibly avoid a fee on your checking account: Shop around for a different bank if your current bank continues to charge you a monthly fee on your account. Be aware of your minimum balance. Many banks offer free checking if you keep at least a certain balance in your account. Make sure you are above this threshold. Sign up for email and text alerts to update you when your balance dips below a certain level. Also see: What the CFPB Has Accomplished in its First 2 Years>> Check into making direct deposits. Some banks offer free checking if your paycheck is deposited automatically. Have multiple accounts at your bank. Your bank wants as much of your business as possible and may offer free services for multiple accounts. Use your bank's ATMs when making withdrawals. The survey of 1,000 adults was conducted in July for the ABA by Ipsos Public Affairs, an independent market research firm.

Friday, January 24, 2014

Finra aims to prohibit brokers' demanding clean records as a condition of settlement

Brokers would not be able to demand that their records be cleared of wrongdoing as a condition of settlement of an investor complaint under a rule being considered by Finra.

The broker-dealer regulator told two lawmakers in a letter released Friday that it intends to reform so-called expungement, the process that allows brokers to sanitize their information in the BrokerCheck online database system.

“We are presently developing rule changes that would prohibit the practice of conditioning settlements on an investor's agreement not to oppose expungement,” Finra Chairman and chief executive Rick Ketchum wrote in a Jan. 6 letter to Sen. Jack Reed, D-R.I., and Sen. Charles Grassley, R-Ia. “While the suggestion to include such conditions in exchange for additional compensation does not always originate with the brokerage firm or broker, this practice may interfere with arbitrators' ability to independently determine the appropriateness of expungement and make the requisite affirmative finding.”

Mr. Ketchum wrote his letter in response to a Dec. 16 letter to Finra from Mr. Reed and Mr. Grassley that questioned its expungement policy. The senators' letter was based on a study released in October by the Public Investors Arbitration Bar Association that showed that expungement requests were granted more than 90% of the time in cases resolved by settlement or stipulated awards between 2007 and 2011.

In his response to the senators, Mr. Ketchum addressed several PIABA recommendations to improve the expungement process. In addition to the settlement rule change, Mr. Ketchum said that Finra is overhauling expungement training for arbitrators. The revised training will be posted on Finra's website next month.

“The training increases the emphasis on the importance of [the Central Registration Depository] and BrokerCheck, and the arbitrator's critical role in maintaining the integrity of disclosure information contained on the system,” Mr. Ketchum wrote.

In recent guidance to arbitrators, Finra underscored the “extraordinary nature of expungement relief” and urged them to consider carefully whether clearing a broker's record could deny important information to investors reviewing an adviser's background, according to Mr. Ketchum.

Mr. Reed and Mr. Grassley, who had pressed Finra on the potential threat to investors posed by expungement, said in a statement Friday that they are happy with Finra's answers.

“Finra was responsive to our inquiry and it appears the organization is taking this problem seriously,” Mr. Reed and Mr. Grassley said. “We will continue to follow up and work closely with Finra to ensure that it follows through on its commitment to improve the expungement system. It is important for consumers to have the unvarnished information they need.”

Although the number of court-approved expungement requests during the period of the PIABA study was only 850, out of 17,635 cases filed, “any inappropriate reduction in the amount of! broker disclosure to investors is of serious concern to Finra,” Mr. Ketchum wrote.

In responding to other PIABA recommendations, Mr. Ketchum said that Finra could not participate in arbitrators' proceedings concerning expungement but noted that all expungement requests are reviewed by Finra and must be approved by a court.

Mr. Ketchum said that Finra has the authority to improve the expungement system without congressional intervention.

“At this stage, Finra does not believe a legislative solution is necessary,” he wrote.

Energy Favorites

Despite impressive gains this year, leading energy stocks remain cheap relative to other market sectors, suggests Robert Rapier. Rather than focus on one specific stock, the editor of The Energy Strategist offers a package of favorite ideas in various energy sub-sectors.

Given the likelihood of continued strength in energy commodity prices, 2014 should prove another fruitful year for these underappreciated overachievers. Below are stock recommendations predicated on our outlook for the energy patch next year.

Natural Gas prices surged recently to an 18-month high, as a cold snap gripping much of the US spurred big withdrawals from storage.

Supply, meanwhile, is constrained by the fact that, even at the current elevated price, few gas projects outside of the bountiful Marcellus shale can compete with the returns available in crude oil. Our favorite Marcellus drillers are Cabot Oil & Gas (COG) and Antero Resources (AR).

Among the alternatives to oil and gas, solar has flashed the most promise of late; coal remains buried in a painful slump, nuclear continues to be dogged by safety issues in the wake of Fukushima, and biofuels remain too unproven and risky as an investment.

We're big fans of solar pioneer First Solar (FSLR), which continues to drive down the cost of photovoltaic cells, to win new business from US utilities.

The coming year looks auspicious for selected refiners. The domestic margin for the refining industry will likely depend on the continuation of recently encouraging US demand trends, and on that score, many refining stocks appear to have priced-in quite a bit on the potential good news.

Our recommended stocks in the camp are HollyFrontier (HFC), Valero (VLO), and Western Refining (WNR).

Subscribe to The Energy Strategist here...

For More 2014 Top Stock Picks

Thursday, January 23, 2014

Americans to Obama: The Economy Is All That Counts

President Obama cannot run for office again, at least not for the presidency. So, the effects of his approval ratings are academic. However, he may care about how he is considered in his second term. If so, all most Americans care about is the health of the economy.

The economy is supposed to be getting better. According to The White House, it is already tremendously better than during the recession. Many Americans do not agree with that assessment. Almost all these people think about is what the economic future of America, and themselves, will be.

According to a new poll from Gallup:

The economy carries the greatest weight of nine key issues in determining how Americans rate President Barack Obama overall. Americans who approve of the job Obama is doing on the economy are six times more likely to approve of Obama’s overall performance than those who disapprove of Obama’s handling of the economy. That is nearly double the impact of any other issue. The next-most-influential issues are healthcare, terrorism, and the federal budget deficit.

“Six times” is not a typographical error.

The opinions of people who are worried about the economy likely rest with job creation and the stagnation of wages. Unemployment at well over 7% remains much higher than what experts believe reflects national economic health. The real wages of Americans who make the national median household income have fallen in the past decade. The prices of most of the things they need to cover daily living expenses have risen.

One of the oddities of the Gallup results is that the deficit is usually tied to the strength of the economy. Many Americans apparently do not believe that, or perhaps do not understand it. Either way, the war in Washington over debt and deficits gets lost as people consider how they live.

Because the cost of health care is so large a part of many people’s overall costs, and people worry about their health in general, one might think it would be higher on the list. Clearly, many Americans set that issue aside, perhaps because they believe they cannot afford good care. Such an assumption is absurd, because it appears thin. However, that does not mean it cannot be true.

The state of the economy was at the top of most people’s lists throughout the recession. Even with what is described by the White House as a recovery, many Americans are not convinced.

Methodology: Results for this Gallup poll are based on telephone interviews conducted Aug. 7 to 11, 2013, with a random sample of 2,059 adults, aged 18 and older, living in all 50 U.S. states and the District of Columbia.

Top 10 Low Price Companies To Buy Right Now

Everything was looking great with my new investment.

The stock had been steadily climbing higher since my purchase in early January. This company was among the original members of the S&P 500 and once ranked among the Dividend Aristocrats. Members of this exclusive list have raised their dividends annually for 25 consecutive years. Talk about a vote of confidence!

However, the company was dropped from that list recently. Not because of an issue with its dividends -- but because it no longer had the minimum $3 billion market capitalization to remain a member.

In addition, sales had been slipping over the past several years. Counterbalancing the bad news, the company was still creating decent cash flow, producing solid returns on invested capital and trading at relatively low price.

Top 10 Low Price Companies To Buy Right Now: Delta Air Lines Inc (DAL)

Delta Air Lines, Inc. (Delta) provides scheduled air transportation for passengers and cargo throughout the United States and around the world. The Company�� route network gives it a presence in every domestic and international market. Delta�� route network is centered around the hub system it operate at airports in Amsterdam, Atlanta, Cincinnati, Detroit, Memphis, Minneapolis-St. Paul, New York-JFK, Paris-Charles de Gaulle, Salt Lake City and Tokyo-Narita. Each of these hub operations includes flights that gather and distribute traffic from markets in the geographic region surrounding the hub to domestic and international cities and to other hubs. The Company�� network is supported by a fleet of aircraft that is varied in terms of size and capabilities.

Delta has bilateral and multilateral marketing alliances with foreign airlines to improve its access to international markets. These arrangements can include code-sharing, reciprocal frequent flyer program benefits, shared or reciprocal access to passenger lounges, joint promotions, common use of airport gates and ticket counters, ticket office co-location, and other marketing agreements. Its international code-sharing agreements enable it to market and sell seats to an expanded number of international destinations. The Company has international codeshare arrangements with Aeromexico, Air France, Air Nigeria, Alitalia, Aeroflot, China Airlines, China Eastern, China Southern, CSA Czech Airlines, KLM Royal Dutch Airlines, Korean Air, Olympic Air, Royal Air Maroc, VRG Linhas Aereas (operating as GOL), Vietnam Airlines, Virgin Australia and WestJet Airlines.

In addition to the Company�� marketing alliance agreements with individual foreign airlines, it is a member of the SkyTeam airline alliance. Delta also has frequent flyer and reciprocal lounge agreements with Hawaiian Airlines, and codesharing agreements with American Eagle Airlines (American Eagle) and Hawaiian Airlines. It has air service agreements with multiple do! mestic regional air carriers that feed traffic to its route system by serving passengers primarily in small-and medium-sized cities.

Through the Company�� regional carrier program, it has contractual arrangements with 10 regional carriers to operate regional jet and, in certain cases, turbo-prop aircraft using its DL designator code. In addition to Delta�� wholly owned subsidiary, Comair, it has contractual arrangements with ExpressJet Airlines, Inc. and SkyWest Airlines, Inc., both subsidiaries of SkyWest, Inc.; Chautauqua Airlines, Inc. and Shuttle America Corporation, both subsidiaries of Republic Airways Holdings, Inc.; Pinnacle Airlines, Inc. and Mesaba Aviation, Inc. (Mesaba), both subsidiaries of Pinnacle Airlines Corp. (Pinnacle); Compass Airlines, Inc. (Compass) and GoJet Airlines, LLC, both subsidiaries of Trans States Holdings, Inc. (Trans States), and American Eagle.

The Company�� SkyMiles program allows program members to earn mileage for travel awards by flying on Delta, Delta�� regional carriers and other participating airlines. Mileage credit may also be earned by using certain services offered by program participants, such as credit card companies, hotels and car rental agencies. In addition, individuals and companies may purchase mileage credits. The Company reserves the right to terminate the program with six months advance notice, and to change the program�� terms and conditions at any time without notice.

SkyMiles program mileage credits can be redeemed for air travel on Delta and participating airlines, for membership in the Company�� Delta Sky Clubs and for other program participant awards. Mileage credits are subject to certain transfer restrictions and travel awards are subject to capacity controlled seating. During the year ended December 31, 2011, program members redeemed more than 275 billion miles in the SkyMiles program for more than 12 million award redemptions. During 2011, 8.2% of revenue miles flown on Delta were from a! ward trav! el.

The Company generates cargo revenues in domestic and international markets through the use of cargo space on regularly scheduled passenger aircraft. Delta is a member of SkyTeam Cargo, an airline cargo alliance. SkyTeam Cargo offers a network spanning six continents and provides customers an international product line.

The Company has several other businesses arising from its airline operations, including aircraft maintenance, repair and overhaul (MRO); staffing services for third parties; vacation wholesale operations, and its private jet operations. Delta�� MRO operation, known as Delta TechOps, is an airline MRO in North America. In addition to providing maintenance and engineering support for its fleet of approximately 775 aircraft, Delta TechOps serves more than 150 aviation and airline customers. Its staffing services business, Delta Global Services, provides staffing services, professional security, training services and aviation solutions to approximately 150 customers. The Company�� vacation wholesale business, MLT Vacations, is the provider of vacation packages in the United States. Its private jet operations, Delta Private Jets, provides aircraft charters, aircraft management and programs allowing members to purchase flight time by the hour.

The Company competes with SkyTeam, United Air Lines, Continental Airlines, Lufthansa German Airlines, Air Canada, American Airlines, British Airways and Qantas.

Advisors' Opinion:- [By Ben Eisen and Saumya Vaishampayan]

Delta Air Lines Inc. (DAL) � climbed 5.2% after the firm said its passenger unit revenue was up 10% in December.

- [By Paul Quintaro]

Shares of Delta Air (NYSE: DAL) are down 3.6 percent at last check, shares of United Continental (NYSE: UAL) are down 3.8 percent, US Air (NYSE: LCC) shares down 2.8 percent, shares of Southwest (NYSE: LUV) down 2 percent, JetBlue (NASDAQ: JBLU) shares down 2 percent and shares of SkyWest (NASDAQ: SKYW) down nearly 4 percent.

- [By Adam Levine-Weinberg]

Delta Air Lines (NYSE: DAL ) is one of the largest and most successful U.S. airlines today. In 2012, the company carried more than 100 million passengers on the way to earning an adjusted profit of $1.55 billion. This strong momentum has led to enviable gains for shareholders: Delta stock has nearly doubled since the beginning of December.

Top 10 Low Price Companies To Buy Right Now: Diana Containerships Inc.(DCIX)

Diana Containerships Inc. owns and operates containerships in Greece. The company engages in the seaborne transportation of semi-finished and finished consumer and industrial products. As of February 23, 2012, its fleet consisted of 8 containerships with a carrying capacity of approximately 32,693 twenty-foot equivalent units. Diana Containerships Inc. was founded in 2010 and is based in Athens, Greece.

Top 10 Insurance Companies For 2014: Macquarie Radio Network Ltd(MRN.AX)

Macquarie Radio Network Limited engages in the radio and associated media activities in Australia. The company offers adult radio audience programs. It also owns a public relations and marketing communications agency, Map and Page; and media Websites, such as 2GB.com, 2CH.com, and rugbyleaguelive. The company is headquartered in Pyrmont, Australia. Macquarie Radio Network Limited is a subsidiary of John Singleton Promotions Pty Limited.

Top 10 Low Price Companies To Buy Right Now: Monument Mining Limited(MMY.V)

Monument Mining Limited, together with its subsidiaries, engages in the acquisition, exploration, development, and operation of gold mineral properties. The company?s principal properties include Selinsing Gold Project, Damar Buffalo Reef Prospect, and Famehub properties are located in the Central Gold Belt of Western Malaysia. It also holds interest in the Mersing Gold Project located in the Jahore State of Malaysia. Monument Mining Limited is headquartered in Vancouver, Canada.

Top 10 Low Price Companies To Buy Right Now: Hilton Metal Forging Ltd (HILTON)

Hilton Metal Forging Limited (HMFL) is an India-based company. The Company produces a range of forgings, flanges and other allied products. The Company is mainly engaged in manufacturing of steel forgings and flanges and forged fittings for oil and gas industry, petrochemicals and refineries. The Company caters to oil and gas sectors, petro chemical and refineries, marine and ship building, paper and pulp, and agricultural sectors. The Company supplies flanges, stub ends, elbows, bonnets, valve body and other forged products.Top 10 Low Price Companies To Buy Right Now: Frank s International NV (FI)

NA

Advisors' Opinion:- [By Jake L'Ecuyer]

Frank's International NV (NYSE: FI) shares tumbled 12.40 percent to $25.86 on Q3 results.

Gol Linhas Aereas Inteligentes (NYSE: GOL) was down, falling 6.31 percent to $4.0850 after the company posted a loss in the third quarter.

- [By Ben Levisohn]

Frank’s International�(FI) has gotten a boost this morning after UBS started coverage of the oil-equipment company’s stock as a Buy. Analyst Angie Sedita�lists the four reasons why she calls the company a “hidden gem:”

Bloomberg(1) Strong company operations – technical strengths, strong execution, above�average margins.

(2) Highly attractive geographic exposure – 74% of revenues are driven by the offshore markets (US and international) and 45% from international activity.

(3) Visible growth profile ��offshore and international markets offers the�highest growth opportunities in the market (ultra-deepwater fleet expected to grow 40% by 2016).

(4) Financial strength ��almost no debt, solid FCF yield (3%) and dividend (1.5% yield).Sedita says the stock could rise to $33, 14% from its last price of $29.06.

Frank’s has gained 3.4% today, while Weatherford (WFT) has gained 0.9% after a Wells Fargo upgrade.�Tesco�(TESO) has dropped 0.2% to $16.52,�Baker Hughes�(BHI) has fallen 0.6% to $49.98 and�National-Oilwell�(NVO) is off 0.5% at $78.48.

- [By Namitha Jagadeesh]

Herro�� fund has beaten 96 percent of its peers in the last five years, data compiled by Bloomberg show. He owns shares in Daimler AG (DAI), the Stuttgart, Germany-based maker of luxury cars, and Fiat Industrial SpA (FI), the maker of commercial and agriculture vehicles spun off from Fiat SpA in 2011.

Top 10 Low Price Companies To Buy Right Now: Edac Technologies Corporation(EDAC)

EDAC Technologies Corporation provides design, manufacturing, and other services to the aerospace and industrial markets. The company produces low pressure turbine cases, hubs, rings, disks, and other complex and close tolerance components for various aircraft engine and ground turbine manufacturers. It also offers rotating components, such as disks, rings, and shafts; provides precision assembly services, including the assembly of jet engine sync rings, aircraft welding and riveting, post-assembly machining, and sutton barrel finishing; and engages in precision machining for the maintenance and repair of components in the aircraft engine industry. In addition, the company designs and manufactures fixtures, precision gauges, close tolerance plastic injection molds, and precision component molds for composite parts and specialized machinery. Further, it designs, manufactures, and repairs various types of precision grinders, as well as precision rolling element bearing spind les, including hydrostatic and other precision rotary devices for machine tool manufacturers, special machine tool builders and integrators, industrial end-users, and powertrain machinery manufacturers and end-users in the United States, Canada, Mexico, Europe, and Asia. The company serves a range of industries in areas, such as special tooling, equipment and gauges, and components used in the manufacture, assembly, and inspection of jet engines. EDAC Technologies Corporation was founded in 1946 and is based in Farmington, Connecticut.

Top 10 Low Price Companies To Buy Right Now: Nemaska Exploration Inc (NMX.V)

Nemaska Lithium Inc. engages in the exploration and development of lithium mining properties in Canada. The company is also involved in processing spodumene into lithium compounds. It holds 100% interests in the Whabouchi property consisting of 33 claims covering an area of approximately 1,716 hectares located in the James Bay area of Quebec province; and the Sirmac property comprising 15 mining claims covering an area of approximately 645 hectares located in the Quebec province. The company was formerly known as Nemaska Exploration Inc. and changed its name to Nemaska Lithium Inc. in December 2011. Nemaska Lithium Inc. is headquartered in Quebec, Canada.

Top 10 Low Price Companies To Buy Right Now: Mawson Resources Ltd(MAW.TO)

Mawson Resources Limited, a development stage company, engages in the acquisition and exploration of mineral properties in Finland, Peru, and Sweden. It explores primarily for gold, uranium, and copper ores. Its principal projects include the Rompas gold and uranium project with 132,890 hectares of claim reservations and 2,539 hectares of claim applications located in municipality of Ylitornio, Finland; and the Alto Quemado gold copper project comprising seven granted mineral concessions totaling 3,800 hectares situated in the Province of Caylloma, Peru. The company was founded in 2004 and is headquartered in Vancouver, Canada.

Top 10 Low Price Companies To Buy Right Now: Dajin Resources Corp (DJI)

Dajin Resources Corp. (Dajin) together with its subsidiaries, is engaged in the acquisition and exploration of mineral properties located in the Province of British Columbia, Canada and Argentina. The Company owns a 100% interest in 29 mineral claims with a 1,500 meter long, linear gold in soils anomaly adjacent to Spanish Mountain Gold Ltd.�� Spanish Mountain gold discovery. The Company also owns a 100% interest in 47 mineral claims in the Addie 2 property which is located south of Quesnel Lake and adjacent to the Frasergold deposit. The Company owns a 65% interest in 32 certain mineral claims and 100% interest in 23 additional minerals claims which make up the Cowtrail Property where Dajin has intersected 1.16 grams per ton gold and 0.043% copper mineralization over 60.0 feet (18.3 meters). The Company holds a 100% interest in concessions or concession applications in Salta and Jujuy Provinces.Wednesday, January 22, 2014

Green Automotive is Locked and Loaded (GACR)

If there was any concern about how Green Automotive Co. (OTCMKTS:GACR) would continue its impressive expansion, that question was answer today. GACR will be issuing debt to raise some capital, taking advantage of the low interest rate environment we're currently in.

The press release announcing the issuance of the fixed income didn't specify how much working capital Green Automotive Company was aiming to raise. But, given that the company's current market cap is $27 million and that the 2012 acquisition of shuttle bus maker Newport Coachworks cost an estimated $13 million, it wouldn't be unreasonable to presume the bond issuance will is on the order of seven figures... if not more.

Given the numbers at hand, it wouldn't be tough to wonder if a seven-figure fund-raiser via a fixed income instrument was a case of Green Automotive Co. biting off more than it can chew, especially knowing last quarter's revenue was only a tad more than $1 million. The past doesn't accurately indicate the future for GACR, however. This is a case where a company is paying to put multiple pieces in place now for strong revenue in the future.

Take the acquisition of bus-maker Newport Coachworks as an example. While Green Automotive Co. had to pay $13 million to bring the company under the GAC umbrella, the company felt then that the electric bus opportunity - via Newport Coachworks - could be worth $37 million in sales per year. So where is that revenue now? It's coming, but the first thing GACR needed to do was re-outfit the production facility and redesign its shuttle buses for battery power. It also needed to take time to redefine itself as an electric bus company to potential vendors. It was time well spent. In the meantime, Don Brown Bus Sales has awarded GAC an order of more than 400 battery-powered buses to be delivered over the course of the next few years.

Point being, Green Automotive Company spends its money well.

GACR isn't just a bus company, however. It also owns an e-car technology company that not only provides maintenance and service for existing EVs, while simultaneously developing some of the technology that will be going into a new EV being designed by an EU consortium. This group of companies should come up with a prototype at some point in 2014, with the vehicle perhaps - realistically - going into production sometime in 2015 or 2016. It takes money to design and build those technologies, however, and there's no immediate payback. There is an eventual payback, however, and considering how well Tesla's multi-year development process has finally paid off, GACR shareholders have plenty to look forward to.

Although Green Automotive Co. didn't say what its plans were for this new cash, more complementary acquisitions are a distinct possibility. The company bought 21% of electric truck maker Viridian Motor Corp. earlier in the month, and though that's technically not a controlling interest, it's certainly an influential interest that may well benefit Viridian as much as it benefits GAC. Indeed, as we've seen from the combination of all of Green Automotives acquisitions this far, the whole is greater than the sum of its parts.

Bottom line? While the prospect of a small company taking on new obligations can be daunting for shareholders, in the case of Green Automotive Company - which has proven it knows how to piece together a company with complementary pieces - the cash injection is actually an exciting prospect.

For more on Green Automotive, visit the SCN research page here.

Tuesday, January 21, 2014

Apple’s Handheld TV, and All the Other Video Devices

How big does a smartphone or tablet screen have to be before it can be considered a TV? Apple Inc. (NASDAQ: AAPL) apparently will test an iPhone with a six-inch screen, according to The Wall Street Journal. However, it is not a tablet, at least as far as the traditional definition of tablets goes. A small step up in size, RCA makes a 13.3 inch television screen. The breadth of screen sizes opens the question of what is a smartphone, a tablet or a TV, and what some can watch based on their deteriorating vision.

Does the screen size debate matter? Yes, to the extent of what people are willing to do with a device. It is assumed that a smartphone is portable enough to carry in a pocket, probably. And a tablet has to fit in a brief case or backpack, perhaps. A television is a free-standing device that has to go on a stand or on a wall, or be suspended by wire from a ceiling.

Another question about screen size is what people will do with a device, what will they use it for? New wearable watches may have screens too small to view anything but video clips. Tablet screens may be too small to watch some HD programs. TVs are bolted-down devices, no matter how well they display video content.

The consumer electronics industry still makes distinctions that may be false, at least as far as many consumers are concerned. That cracks open the door to whether definition matters in a world in which the utility of screen size is more a matter of what content it can play and the extent to which the display is acceptable to consumers.

It may be that the only line of demarcation left in the spectrum from video watches to televisions is price. Perhaps consumers believe that the larger the screen, the more they will need to pay. That line has been blurred, too. Philips makes a 32-inch screen that retails for $450 (used) on Amazon.com Inc. (NASDAQ: AMZN). As a matter for fact, Amazon may be the largest warehouse of video devices. It sells the tiny Samsung Rugby III handset and television screens of more than 70 inches.

The line between video viewing devices already has disappeared to the point where size matters less and less. The definition probably is based on whether consumers believe that labels mean anything as video devices grow bother larger and smaller. Perhaps the line that gets drawn is based on age. People older than 65 own televisions in greater numbers than smartphones. However, for older people, the definition may not matter either. They just cannot see small screens as their vision gets worse. Otherwise, they might want that six-inch screen iPhone just like everyone else does.

Union Pacific Corp.

My top pick for 2014 links the Pacific Coast and Gulf Coast ports with the Midwest and eastern United States gateways, through a rail network of over 31,000 route miles, explains dividend and value investing expert Kelley Wright, editor of Investment Quality Trends.

Union Pacific Corp. (UNP) provides freight transportation services for a wide variety of products and industries, that includes agriculture, food and beverage, automotive parts and materials, finished vehicles, and industrial and construction materials and products.

More importantly, the company provides transportation services for the petrochemical industry, which includes industrial chemicals, plastics, crude oil, and liquid petroleum gases; fertilizers, soda ash, and energy products comprising coal and petroleum coke.

It is the transportation of crude oil and petroleum products that we believe will be the major driver of revenues for the company.

As energy production increases in North America, the lack of pipelines makes the UNP rail network the major transportation conduit to refineries and shipping ports.

UNP offers good historic value when the dividend yield is 2.30% or higher. Based on the current cash dividend of $3.16, a 2.30% dividend yield is realized at $137.

Trading recently around $166 per share, the stock is in its Rising Trend, and we doubt it will fall close to its Undervalue area. That being said, we believe the company still offers good long-term upside potential.

Subscribe to Investment Quality Trends here...

For More 2014 Top Stock Picks

Monday, January 20, 2014

Toyota Gets Aggressive With Its New Corolla

Toyota's new Corolla, shown here in sporty "S" trim, is much more sharply styled than its predecessor. Toyota announced aggressive pricing for the new Corolla this past week. Photo credit: Toyota

Toyota's (NYSE: TM ) Corolla is one of the world's best-selling cars, and the company hopes to build on that success with this all-new version, which will be at U.S. dealers soon. The company announced U.S. pricing for its mainstay compact this past week, and to no surprise, Toyota appears determined to offer good value -- and to undercut the Corolla's biggest global rival, Ford's (NYSE: F ) Focus.

Will the new Corolla help Toyota regain lost ground in the U.S.? In this video, Fool contributor John Rosevear looks at how the new car stacks up -- and gives his thoughts on whether it will succeed in what has become a fiercely competitive market segment.

Ford shareholders have already been rewarded as the Blue Oval has gained ground on Toyota this year. But for Ford's stock to really soar, a few more critical things need to fall into place. In The Motley Fool's special free report entitled, "5 Secrets to Ford's Future" we outline the key factors every Ford investor needs to watch. Just click here now for your free report.

Saturday, January 18, 2014

5 rules of thumb for your money

Please note: Everybody's financial situation is unique- a rule of thumb is only a broad indicator and does not replace a personalized solution. A rule of thumb may or may not be correct for your specific financial situation.

(Read our article titled 5 Personal Finance Tips for Before You Turn 40 )

1. How long will it take to double my money?

Have you ever had an investment salesperson insist that you must buy a certain product because it would double your money in 10 years? The next time this happens to you- do a small calculation to show the salesperson that you know more than he thinks!

The Rule of 72 helps you to calculate what rate of return it requires to double your money in a certain number of years. Alternatively, it can be used to show what number of years it will require to double your money at a particular given rate of return.

Here is how it works: Rate of Return required to double your money = 72 / Number of years

In the above salesperson example, a product that doubles your money in 10 years is giving you an annual rate of return of 7.20% i.e. 72 / 10.

With a 10 year investment horizon you might be better off investing the money into equity yourself and earning a higher rate of return over the 10 year period.

Similarly, Number of years required to double your money = 72 / Rate of Return

If you are earning say 15% on an investment, you can expect your invested money to double in 72/15 years i.e. 4 years and 10 months.

Remember however that the Rule of 72 is only a very broad approximation of the actual answer. To get a more accurate answer, use the number 69 instead of 72. The number 72 is used only because it is easily divisible by many numbers.

(Read about the Rule of 69 )

2. How much equity exposure should I have?

The broad rule is that your equity exposure should be equal to 100 minus your age. So if you are 35 years old, the equity component of your overall portfolio should be (100- 35)% = 65%.

However, this rule is again very broad and differs from situation to situation.

For example, if you have high liabilities and expensive financial goals that are coming up within the next 3 years, then the corpus for these expenses and goals should not be in equity, it should be in debt i.e. fixed income- or else with any major market volatility, the goals will be jeopardized. So keep your goal horizon in mind too.

Related News

Risk-return relationship: High return is the risk premium Would falling rupee make bank FDs attractive?Friday, January 17, 2014

Ericsson CEO could be vying for Microsoft job

Vestberg, 48, is a former elite-level handball player, so he's got the competitive chops. He's known as something of a media-wise tech geek.

A large contingent of U.S. tech industry and Wall Street analysts expect Microsoft to stay in house, with senior Microsoft execs Satya Nadella, Stephen Elop and Tony Bates viewed as front runners to replace Ballmer.

More: Why Microsoft should stick with internal candidates

So Vestberg's name surfacing is something of a surprise, underscoring the dilemma Microsoft's board faces. Will they play it safe -- or shake things up and go with fresh, outside blood?

Vestberg worked his way up the ranks to CFO and become CEO at Ericsson in 2010. Under his watch the company has lost ground to Asian rivals.

Vestberg's shortcomings are said to include few recent successes in the rough and tumble consumer products mobile devices market, where Korea's Samsung and China's Huawei are dominating.

There appears to be plenty of time for candidates to maneuver for the top job at the world's largest software company. If Bloombergs' insider sources are to be believed, Microsoft won't name Ballmer's replacement until the last week of January, at the earliest. Ericsson and Microsoft, of course, aren't commenting.

Thursday, January 16, 2014

Hot Cheap Companies To Own For 2014

Investors and politicians have been debating the merits of solar power for decades. In the late '70s and early '80s, the industry went through a boom because of government subsidies that were extremely short-lived, and it took until a subsidy-driven boom in Germany in the early 2000s to get back on the map again. Solar power was always a pipe dream that couldn't get off the ground, unable to compete with fossil fuels that were cheap and plentiful.

But over the past decade, the narrative has changed. Today, solar power is becoming a force in energy, and while subsidies play a role in solar energy's growth, it's the falling cost of solar power that's driving the boom. Like it or not, solar power is here to stay.

The U.S. begins to see the light

The entrenched energy industry and political powers in the U.S. have been fighting any assistance to the solar industry, but their efforts have failed to slow down its growing momentum. Last year, Congress failed to extend the 1603 Treasury Grant program -- a 30% cash grant given to anyone who installed solar -- cutting one of the main subsidies to the industry. Solar installers were still left with an investment tax credit, but that requires taxable income, creating a financing challenge. �

Hot Cheap Companies To Own For 2014: Oracle Corporation(ORCL)